miriam-doerr/iStock via Getty Images

EZCORP, Inc. (NASDAQ: EZPW) operates more than 1,150 pawn shops in the United States and Latin America. This is a segment known to be relatively counter-cyclical, which means companies can take advantage of weaker economic conditions. Indeed, the attraction of pawnbrokers is that they represent a finance alternative for cash-strapped consumers while providing an affordable retail option with a selection of pawned pre-owned merchandise.

We last covered the stock with an article in February that highlighted a bullish case in a changing macro landscape and rising inflation. In many respects, the outlook for businesses has progressed better than expected over the past few months. Our tracking coverage today recaps the latest quarterly report as EZPW shares have outperformed this year. We reaffirm our buy rating on EZCorp as the stock remains undervalued with more upside benefiting from several growth tailwinds.

Looking for Alpha

EZPW Revenue Summary

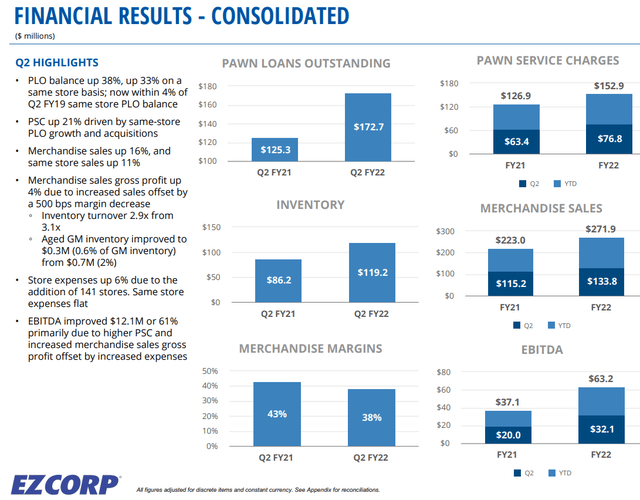

The company announced its fiscal second quarter results on May 4 with non-GAAP EPS of $0.22, $0.08 ahead of estimates. Revenue of $216 million was up 17% year over year and also exceeded expectations by $6 million. It was an otherwise strong quarter, driven by strength in core pledged loans (PLOs) outstanding which climbed 38% year-on-year to $173 million.

The balance of the PLO is a key metric for the company, as it generates high-margin pawnbrokerage (PSC) fees that account for about 35% of total revenue. In terms, the higher level of pawn activity brings in new merchandise that is sold in stores. PSC climbed 21% year-over-year in Q2, while merchandise sales were up 16% and 11% same-store.

Company IR

By segment, operations in Latin America were a growth engine, with net sales increasing 30% year-on-year in the second quarter, compared to 10% in the United States. A theme for the business is that while merchandise margins between Latin America and the United States are below trends in 2021, revenue momentum with particular strength at PSC in both segments has made increase profits.

Company-wide adjusted EBITDA of $32.1 million increased 61% from Q2 2021. This also reflects a cost reduction effort and tight expense control. Store spending as a percentage of revenue at 70% year over year was down from 78% in the second quarter of last year. The general trends here confirm the early success of the company’s “Strengthen The Core” strategic plan put in place at the end of 2020 to grow and generate higher returns.

Company IR

Finally, note that EZCorp ended the quarter with $264 million in cash and cash equivalents, including restricted cash versus $312 million in long-term debt. With an adjusted EBITDA of $93 million in the past year, we consider net debt to an adjusted EBITDA leverage ratio of 0.5x represents a strong balance sheet and liquidity position. The company announced a new $50 million stock buyback authorization citing what it believes to be attractive stock valuations. We agree.

Is EZPW a good investment?

There’s a lot to like about EZCorp which was an exception this year to the stock market’s sell-off. Compared to the stimulus-induced pandemic impulse in 2020 and 2021, all indications are that the economy has teetered between weaker economic growth and historically high inflation. For a large segment of the population defined by subprime credit scores or who are underserved by traditional banking products, pawnbrokers can be a good option to meet cash flow needs.

In our view, last quarter results, especially with growing PLO balances, reflect some of this momentum. In addition, other types of services like payday loans and check cashing also benefit. On the retail side, EZCorp stores can fill the space for price-conscious consumers with quality used merchandise.

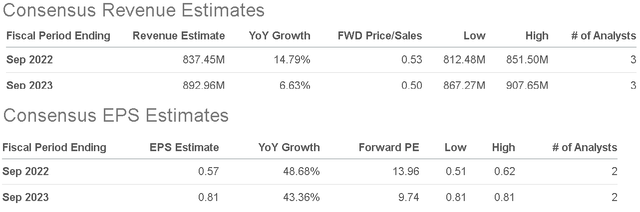

While the company is not providing financial guidance, comments from the most recent earnings conference call hinted at a sense of confidence. The market expects EZPW’s full-year revenue to reach $837 million, a year-on-year increase of 15%. EPS is expected to accelerate higher towards $0.57 based on spending control efforts and also the higher contribution from pawnbrokers this year. We believe that EZCorp can outperform estimates over the next two quarters in terms of growth and margins under the stock’s bullish scenario.

Looking for Alpha

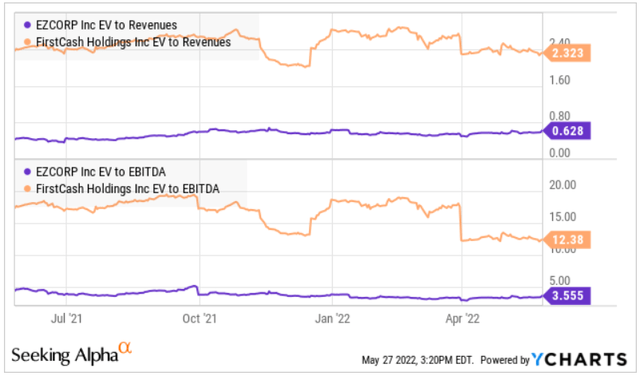

Regarding valuation, the first point to note is that EZPW at an EV of 0.6x to generate multiple incomes at a steep discount to 2.3x of its counterpart and larger competitor in FirstCash Holdings, Inc (FCFS). Similarly, EZPW at an EV/EBITDA multiple of 3.6x is well below 12.4x for FirstCash.

Y-Charts

There are several reasons for this discrepancy, which is partly justified. One of the problems is that EZCorp’s executive chairman, Phillip Cohen, controls 100% of the voting shares. This is often cited as a weakness in corporate governance, as Mr. Cohen effectively has full and exclusive control of the company as it relates to the board of directors. That said, it’s not a deal breaker in our view, as it’s in his interest for the company to succeed.

Other than that, FirstCash and EZCorp have a similar operating strategy between North and South America locations. FirstCash is bigger with more than double the number of stores and also pays a quarterly dividend. On the other hand, FirstCash is highly leveraged with more debt and which is a weakness in its financial profile in our opinion. Acknowledging all of these points, we contend that EZCorp is still undervalued and the valuation gap may narrow to FCFP as an upside catalyst for the stock.

Looking for Alpha

EZPW Stock Price Prediction

We rate EZPW as a buy with a price target of $10.00 for the year ahead, representing a forward P/E of 18x on the current 2022 EPS consensus of $0.57. This is a level the stock last traded at in Q4 2019 before the pandemic and we can say now that the outlook for the company is better than ever. Continued growth efforts, including digital initiatives and improved financial efficiency, support a positive long-term outlook as EZCorp consolidates market share.

The main risk to take into account is at the execution level. Weaker-than-expected trends over the next few quarters could force a reassessment of the earnings outlook. Although the current macroeconomic environment could be positive for pawnbroking, a deeper deterioration in consumer spending and the labor market would affect the stock, limiting its growth opportunities. Pawnbroker balances as well as financial margins are a key control point.